Distillery Boom – Two Decades of Explosive Growth

In the year 2000, you could count the number of American whiskey distilleries on your fingers and toes – barely more than a few dozen nationwide[1]. Fast forward to the 2020s, and the scene has transformed beyond recognition. The craft distilling revolution that took off in the mid-2000s has led to an explosion in new distilleries and brands. By 2010 there were roughly 150–200 distilleries; by 2015 that number had surged past 500[2]. In 2023, estimates suggest the United States hosts well over 3,000 distilleries[3] – a staggering rise from the “handful” operating at the turn of the millennium1. In fact, by 2017 the count of craft distilleries alone had surpassed 1,589, and as of 2022 there were about 2,753 active craft distillers across the country[4].

This craft boom has been accompanied by a proliferation of new whiskey brands. It’s not just longtime Kentucky stalwarts anymore – every state now boasts local whiskey labels, and independent bottlers are sourcing barrels to launch niche brands seemingly every week. The total number of American whiskey products on the market is hard to pin down, but consumers and collectors have watched the shelf space explode with new names. For context, between 2000 and 2022, over 2,000 new whiskey-producing distilleries were established, each often creating multiple brands. The result is a saturated field of thousands of bourbon, rye, single malt, and blended American whiskey labels competing for attention. It’s a far cry from the days when a few big Kentucky and Tennessee names dominated the market.

Historically, American distilling has come full circle. Before Prohibition, the nation had thousands of distilleries; by the late 20th century, consolidation and a whiskey slump left only a few survivors (at one point, reportedly as few as six major whiskey distilleries remained)5. Around the year 2000, the count was still under a hundred. But since then, legal changes and entrepreneurial fervor opened the floodgates, and the number of U.S. distilleries rocketed back into the thousands. In short, America is, or perhaps was, in the midst of a whiskey gold rush, with new distilleries and brands appearing at a pace not seen in over a century.

The big question: is all that new liquid gold finding enough willing throats to drink it and making craft distilleries viable businesses?

Let’s look at the year 2018, EU tariffs implemented but pre covid-19, where the American Craft Spirits Association (ACSA) saw an increase in craft distilleries grow to 1,835 from 1,589 in the year prior[5], with said distilleries producing 3.9% of American production volume and taking up 5.8% of revenue for the year.

· Craft Distillery Definition: Defined as distilleries producing fewer than 750,000 proof gallons annually, equivalent to approximately 1.6 million liters.

Annual Spirits Revenue: $27.6 Billion

American Whiskey Revenue: $3.6 Billion

Craft Distillery Revenue: $209 Million

2018 Average Revenue Per Craft Distillery: $113,787

David vs. Goliath – Craft Distilleries vs. Industry Giants

The production scale of America’s whiskey makers now spans a jaw-dropping range. On one end are the craft upstarts – often tiny outfits with a single pot still, putting out a barrel or two per day (if that). On the other end are the industry giants – think Jim Beam, Jack Daniel’s, Heaven Hill, Sazerac (Buffalo Trace), or MGP Ingredients – whose column stills run 24/7 churning out hundreds or even thousands of barrels daily. The contrast is stark: “There’s no ambiguity between who is a commercial distiller and a craft distiller,” as one observer put it. The “13 legacy distilleries” in the U.S. (the longtime majors) each produce hundreds of barrels per day, “if not more”, while many craft producers make only about one barrel a day on their small stills[6].

To picture it: a large Kentucky bourbon plant or MGP’s Indiana distillery employs towering continuous column stills – industrial hardware stories tall – capable of producing high-proof whiskey in a continuous flow. These behemoths can fill dozens of new charred oak barrels every hour. In fact, Buffalo Trace (owned by Sazerac) recently completed a $1.2 billion expansion that will double its capacity to over 2,000 barrels per day[7]. MGP of Indiana, the source of countless sourced bourbons and ryes, also expanded with new warehouses to stockpile its output6. Meanwhile, the craft guys often use copper pot stills and handcraft spirits in small batches. A distillery with a 250-gallon pot still might labor all day to produce enough newmake to fill a single 53-gallon barrel. Many of these small operations are essentially micro-manufacturing sites – more akin to craft breweries – while the big boys are bona fide factories in scale.

The output numbers drive this home. According to the American Craft Spirits Association, 90% of U.S. craft distillers are very small, producing under 10,000 proof gallons per year (~38k liters), and collectively they account for only about 11.7% of all craft spirits volume sold[8]. In contrast, a mere 1.6% of craft producers are “large” (by craft standards, making 100k–750k proof gallons), yet those few players deliver 57% of the craft case volume. And that’s just within the craft segment – add in the true giants (who each can produce millions of proof gallons annually), and the disparity becomes astronomical. The bottom line: most new distilleries are tiny in output, and while there are thousands of them, their cumulative production is still only a drop in the bucket next to the well-oiled output of legacy producers.

This dynamic also reflects in how whiskey is made and sold. Big distillers with their continuous column stills achieve economies of scale and consistency that allow them to sell a bottle of standard bourbon for $25 and still profit. Craft distillers, often using slower pot still distillation, may have higher cost per bottle and lean on premium pricing or local market appeal to survive. Some craft operations don’t even attempt to produce all their own whiskey at first – they source bulk whiskey from companies like MGP to bottle under their brand, bridging the gap until their home-distilled spirit has aged. It’s an ironic symbiosis: the craft boom was in part jump-started by MGP and other large distillers selling excess barrels to newcomers. The Goliaths supplied the slings to David, so to speak. But as we’ll see, that rampant sourcing and brand launching feeds into the oversupply concerns.

Let’s re-tool those 2018 Numbers now:

90% of Craft Distillers: 1,651

11.7% of Revenue: $24.45 Million

Average Whiskey Bottle Sales Revenue for 90% of Craft Distilleries:

Only $14,811

Production vs. Demand – Is the Whiskey Boom Overshooting?

It’s one thing to build distilleries and fill barrels; it’s another to actually drink all that whiskey. So, has America’s (and the world’s) whiskey thirst kept pace with this supply surge? By some metrics, demand has grown impressively – but still nowhere near the exponential rise in producers and capacity. U.S. consumption of American whiskey (bourbon, Tennessee whiskey, rye, etc.) has indeed been climbing steadily for two decades. In 2023, Americans purchased over 31 million 9-liter cases of American whiskey – 132% more than in 2003[9]. Revenue to distillers from those sales was about $5.3 billion in 2023, more than double the early-2000s level. After losing favor in the late 20th century, bourbon and its cousins have staged a renaissance. The era of the “old man’s drink” stereotype is over – bourbon and rye are in vogue with millennials, cocktail enthusiasts, and collectors alike.

However, supply-side growth has far outstripped these consumption gains. A 132% increase in sales over ~20 years is solid, but recall that the number of distilleries jumped by several thousand percent in the same period. Production volume, particularly capacity, has ballooned. Kentucky’s Bourbon Belt is producing record quantities – the Kentucky Distillers’ Association noted bourbon inventory (barrels aging in Kentucky) topped 11 million barrels in recent years, the highest since records began. Major distillers are cranking out whiskey at a breakneck pace, and craft distillers collectively add to the total (even if their individual shares are small). All this raises a concern:

Are we brewing up our own 21st-century Whiskey Loch?

During the whiskey shortage fears of the mid-2010s, distillers big and small over-indexed on growth, laying down stocks for the future. Now some indicators suggest demand growth is cooling. Industry data in 2023 showed a slight volume decline of –1% for American whiskey in the US (especially in lower-priced tiers), and 2024’s first half continued with a ~–2% volume slip[10]. In other words, domestic demand may have hit a plateau after years of robust expansion. Yet distilleries continued to produce as if the party would never end. This mismatch between optimistic production and leveling demand is classic prelude to a glut. Barrels are maturing in warehouses faster than consumers are emptying bottles on the shelf.

From a revenue perspective, the overall spirits sector in the U.S. just reached a milestone: spirits surpassed beer in market share for the first time in 2022–23. But that victory was led largely by tequila/mezcal and high-end imports – whiskey, while still growing in premium segments, isn’t accelerating like it was a decade ago. Craft distillers, in particular, face an uphill battle. They’ve gained only a 4.9% volume share of the U.S. spirits market so far4. Even with whiskey’s boom, the plethora of new brands are mostly splitting a small slice of the pie. It doesn’t help that the pandemic and tariffs threw curveballs, temporarily stalling on-premise sales and exports in late 2010s.

The key point for investors eyeing whiskey is that supply is beginning to overshoot demand. Inventories of aging whiskey are swelling. In fact, some major producers are blinking: MGP, the source of so much sourced bourbon, recently announced it will scale back whiskey production in 2025 due to “softening” demand and elevated industry-wide barrel inventories10. When a company whose business is selling bulk whiskey decides to pump the brakes, you know the glut fears are real. Analysts have started using the “G-word” (“glut”) and comparing today’s exuberance to past cycles. We are already seeing price pressures – sourced barrel prices that were sky-high a couple years ago are reportedly coming down as buyers become more scarce, and some sourced brands are struggling to gain traction in a crowded market. In summary, the growth in American whiskey output – thousands of new distilleries and brand extensions galore – is increasingly out of sync with the growth in actual whiskey consumption. And that’s a warning sign.

Global Footprint – American Whiskey vs. Scotch Whisky

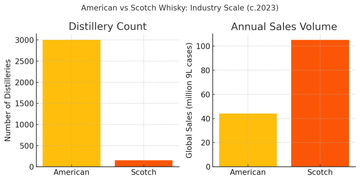

Whiskey may be a global spirit, but not all whiskey industries are equal on the world stage. Scotch whisky, with roughly 150 operating distilleries in Scotland[11], still utterly dominates global brown spirits sales. In 2022, Scotch exports hit a record high, topping £6 billion (around $7.5 billion) in value[12]. That equates to on the order of 1.3–1.4 billion bottles shipped abroad annually– an ocean of Scotch that dwarfs the export volume of American whiskey. By contrast, American whiskey exports in 2023 (which include bourbon, Tennessee, rye, etc.) reached a record of about $1.4 billion[13]– healthy, but just a fraction of Scotch’s figure. In terms of volume, the U.S. exported roughly 177 million liters of whiskey in 2023, whereas Scotch moves nearly a billion liters per year in exports.

The discrepancy is even more striking considering how many more producers America has now. Scotland’s ~150 distilleries (most of them quite small, by the way) collectively outsell the output of America’s 2,000+ distilleries on the global market many times over. Scotch has had a century-long head start in building international distribution and brand prestige. Iconic Scotch brands enjoy entrenched positions in Europe, Asia, and beyond, often backed by multinational liquor conglomerates. American whiskey, while gaining fans overseas, still plays catch-up; the biggest markets for bourbon are actually domestic, with notable export markets in Japan, Europe, and Australia, but nowhere near Scotch’s penetration. The U.S.–EU trade disputes between 2018–2021 (when retaliatory tariffs hit American whiskey) also knocked exports off balance, showing how contingent our export growth is. (Those tariffs caused American whiskey exports to the EU to plunge, only recovering after suspension of the duties[14].)

Why does this matter for a whiskey glut discussion? Because American distillers can’t simply export away their surplus if domestic demand falters. The world market can absorb only so much, and Scotch (along with Irish, Canadian, and Japanese whisky) fiercely guards its turf. In fact, even Scotch is experiencing headwinds now – the famed industry had an 18% drop in export value in early 2024 as some markets cooled off10. The Scotch industry is all too familiar with boom-bust cycles. In the 1980s, they suffered the infamous “Whisky Loch” – a lake of overstocked Scotch that built up when global demand crashed. Producers had been overly optimistic (sounds familiar?) and kept churning out spirit only to find the market swimming in excess. The result: prices tanked and dozens of distilleries were forced to close in the 1980s14. Many of those mothballed Scotch distilleries stayed silent for decades (some never reopened), and the era became a cautionary tale for the whiskey world.

American whiskey’s current situation has parallels to the Scotch Whisky Loch. Rapid capacity expansion, startups by the dozen, and exuberant projections of endless growth – all facing the reality of a finite market. The U.S. isn’t at crisis levels yet, but the warning signs are blinking. Global liquor demand is cyclical; tastes change, recessions hit, fads come and go. If a downturn or even a leveling off meets a huge wave of new American whiskey hitting the market, we could see our own glut – a Bourbon “Lake” to go with the Scotch “Loch”. American producers would then be competing not just with each other, but with a world flooded by surplus spirit. The Scotch industry learned the hard way that whiskey ages in barrels, but demand doesn’t always age like fine wine – sometimes it turns sour. The U.S. craft sector and new distillers haven’t lived through that kind of bust before. Global sales might not be their savior, especially when Scotch (with its far bigger established base but only ~150 distilleries) has shown that even it isn’t immune to overproduction.

The 10-Year Gamble – Does the Old Model Still Work?

Conventional wisdom in the whiskey business long held that if you start a distillery, you’re in for the long haul – a decade, typically, before you really start seeing a return. This 10-year rule comes from the simple fact that good whiskey takes years to mature. You sink capital into equipment, grains, barrels, and you wait while the angels take their share of your inventory evaporating in the warehouse. A famous industry quip: “If most businesses plan to lose money for three years, a whiskey startup should plan for ten”6. Indeed, that was the craft distiller’s dilemma: how to survive the lean years of laying down stock. Many solved it by releasing unaged spirits (gin, vodka) for quick cash, or sourcing ready-made bourbon to bottle under their label. Essentially, they tried to cheat time – because waiting 6–8 years for your first straight bourbon to fully mature without revenue is a rich man’s game.

But in a saturated market, the 10-year path to payoff looks more like a tightrope walk. The new reality is that even if you make it to year ten, you’ll be entering a market crowded with hundreds of other 10-year-old craft whiskeys and thousands of sourced NDP (non-distiller producer) brands. The days when a craft distiller could assume “if we build it (and age it), they will come” are fading. Not everyone will make it to profitable maturity – some are likely to get weeded out much sooner. We’ve already seen craft distilleries put up for sale or quietly shuttered when the cash burn was too high. The ones that do survive are often those that diversified their business model: heavy tourism focus, tasting room sales, contract distilling for others, or attracting investors who don’t mind a very long-term play.

Consider that many craft distillers rely heavily on direct sales and local markets to stay afloat. In 2019, nearly half (47%) of small craft distillers’ sales were right from their own distillery premises (tasting rooms, etc.), not through wide distribution[15]. That works when you’re a local novelty – but as more distilleries sprout, even the local support gets divided. How many hometown whiskey tours and limited-edition bottle sales can the average consumer partake in? There’s a hint of saturation even at the tourism level in Kentucky, where the Bourbon Trail is booming but every new distillery is vying to become a destination.

Most tellingly, the current scramble has even changed the incentives for new distilleries. Rather than waiting 6–10 years to prove themselves, some new ventures aim to flip faster: build a brand and a bit of inventory, then sell the company to a larger player looking to acquire brands (I’ve seen acquisitions of a few high-profile craft distillers by big liquor companies in recent years). Others are embracing the trend of cask sales to investors to raise capital. This is epitomized by firms like CaskX, which pitch whiskey barrels as appreciating assets you can buy now and sell later. It’s a novel funding model – effectively getting whiskey enthusiasts/investors to bankroll the aging process, on the promise that the whiskey in the barrel will be worth significantly more in 5-10 years.

It sounds like a win-win: the distillery gets cash upfront, the investor gets to own a “slice” of the future whiskey bonanza. But herein lies the skepticism that underpins this entire analysis: Will those casks actually be worth more in the future, or are we staring at fool’s gold? If production continues to overshoot and a glut forms, the value of aging whiskey could stagnate or even drop. In the worst case, one might end up with a barrel of bourbon that’s harder to sell than a crate of overripe bananas. Remember the Whisky Loch – back then, excess barrels weren’t treasures; they were burdens sold off cheap or poured down the drain. As one whiskey investment analyst wryly noted, “If whiskey production outpaces drinkers, barrels can become about as valuable as a doorstop.”[16] In other words, without a market of thirsty buyers, that fancy 10-year-old craft bourbon barrel someone bought via a CaskX investment could turn into a very expensive oak paperweight.

The traditional 10-year business model is being stress-tested like never before. It still holds true that making quality aged whiskey requires patience. What’s changed is the market context in which that aged whiskey will emerge. Ten years ago, a new distillery could dream that in a decade, whiskey demand would be even higher and their matured product would fetch top dollar (especially as a craft curiosity). Many today are finding that by the time their whiskey is ready, the shelves are already full of other 5-, 6-, 8-, 10-year-old whiskeys from countless sources. To succeed now, a distillery can’t just make good juice and wait – it needs a strong brand story, differentiation (unique mashbills, local grain, innovative styles), and savvy marketing to carve out a niche in a crowded field. Either that or have a very loyal local following that will buy most of what you produce at a premium price.

For investors, the takeaway is clear: American whiskey is not a guaranteed goldmine. The industry’s growth has been spectacular, but trees don’t grow to the sky. The current data hints at oversupply, and history (both Scotch’s and Bourbon’s) teaches us that whiskey booms can and do bust. American whiskey’s boom has been a fun ride – new distilleries popping like mushrooms and barrel prices soaring – but when growth in consumption lags growth in production, something’s got to give. We may well see a shakeout where only the stronger brands and distillers thrive, while others liquidate stocks at discounts.

In conclusion

Rising production alone does not justify rising cask values – not unless that production is matched by even greater rising demand. Right now, the excitement (and hype) around whiskey cask and distillery investing has inflated cask prices on the expectation that today’s scarce bottles will be even scarcer tomorrow. Yet with so much whiskey in the pipeline, tomorrow’s scarcity is far from guaranteed. The American whiskey industry is entering a new phase of maturity and possibly saturation. For those betting big on barrels of bourbon as “liquid gold,” it’s wise to remember that gold can turn to fool’s gold when the market overheats. Skepticism, in this case, is a whiskey lover’s healthiest pour. Will the boom sustain or are we brewing a new whiskey lake? The answer will determine whether all those newly filled casks aging in Kentucky and Indiana rickhouses become prized assets – or cautionary tales floating in a whisky loch of our own making.

[1] https://whiskyadvocate.com/bourbon-timeline

[2] https://www.bls.gov/spotlight/2023/a-look-at-a-neat-industry-distilleries/

[3] https://www.parkstreet.com/u-s-craft-spirits-category-worth-7-8-billion-in-2023

[4] https://www.whiskymag.com/articles/american-craft-distillers-leading-growth-in-us-spirits-industry-report-finds/

[5] https://americancraftspirits.org/wp-content/uploads/2017/02/ACSA-2019-Annual-Report.pdf

[6] https://www.cincinnatimagazine.com/high-spirits-blog/mgp-ingredients-lawrenceburg

[7] https://www.distillerytrail.com/blog/buffalo-trace-distillery-production-up-50-as-1-2-billion-expansion-continues-capacity-to-double-to-2000-barrels-day-by-year-end/

[8] https://americancraftspirits.org/wp-content/uploads/2017/02/Preliminary-Draft-2020_Craft-Spirits-Data-Project-compressed.pdf

[9] https://www.distilledspirits.org/wp-content/uploads/2024/02/2023-American-Whiskey-Fact-Sheet-NEW1.pdf

[10] https://www.ohbev.com/blog/whiskey-market-forecasts-and-trends

[11] https://en.wikipedia.org/wiki/List_of_whisky_distilleries_in_Scotland

[12] https://whiskyadvocate.com/U-S-Scotch-Whisky-Imports-Rise-In-Volume-Dip-In-Value-In-2024

[13] https://spectrumnews1.com/ky/louisville/news/2024/02/28/us-spirits-exports-american-whiskeys-2023

[14] https://vinepair.com/articles/whisky-loch

[15] https://americancraftspirits.org/wp-content/uploads/2017/02/Preliminary-Draft-2020_Craft-Spirits-Data-Project-compressed.pdf

[16] https://www.linkedin.com/pulse/part-1-hype-vs-history-debunking-guaranteed-returns-whisky-qwuxc/

Disclaimer: The data presented in this article comes from a variety of sources ranging from private market research firms to government agencies. Given the discrepancies in reporting between entities like the TTB and other regulatory bodies, The Whiskey Lab prioritizes information from private entities trusted within the community. Our analysis reflects this choice, aiming to provide the most reliable insight available.

Closing Note: Thank you for joining us on this detailed exploration of the American whiskey industry. This article is not intended as a critique of American distillers but rather as a candid look at the economics shaping their world. While small local craft distilleries can significantly benefit local economies and thrive through various revenue streams, relying solely on the national sale of whiskey produced from small-scale operations under 40,000 liters annually may not be feasible. We celebrate the diversity and creativity of these small producers and recognize their valuable contribution to our communities and culture.